Retirement marks the culmination of decades of saving and investing. As you transition from wealth accumulation to wealth preservation, understanding how to manage risks becomes paramount. Without a clear risk management plan, retirees may overspend, inadvertently lock in losses, or miss opportunities for growth.

In this article, you27ll discover practical strategies and expert principles to build a well-diversified across multiple asset classes retirement portfolios that balance growth, income, and capital preservation.

Common Risks Retirees Face

Even the most diligent savers encounter pitfalls that can erode their nest egg. Awareness of these risks is the first step toward mitigation.

- Overspending early in retirement can deplete resources too quickly.

- Investing too conservatively may lead to insufficient growth to outpace inflation.

- Unexpected deviation from a financial plan often stems from emotional reactions to market volatility.

- Market downturns can sharply reduce portfolio value during critical withdrawal phases.

Assessing and Reassessing Risk Tolerance

Risk tolerance is not static. As you draw closer to or enter retirement, your capacity to absorb losses diminishes. Younger investors often embrace higher volatility for greater long-term returns, while retirees prioritize preservation.

Implement systematic portfolio reviews at least annually to ensure your investments align with your evolving comfort level. Incorporate cash or short-term bonds covering one to four years of living expenses. These reserves allow you to maintain cash for downturn protection and avoid forced selling under adverse market conditions.

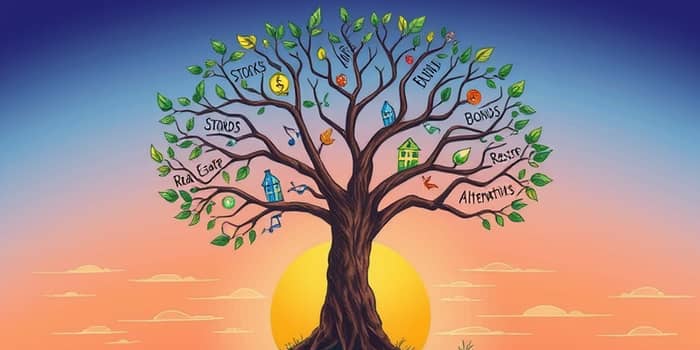

Building a Diversified Portfolio

Diversification spreads risk across various asset classes, cushioning the impact when a particular sector underperforms. A well-balanced structure adapts over time, shifting from growth-focused in early years to income-oriented in retirement.

- Equities for inflation protection and long-term growth

- Investment-grade bonds for steady income and downside cushioning

- Real estate or REITs to add tangible asset exposure

- Alternative investments such as precious metals or commodity leases

Align your investments with goals by adjusting allocations every few years or when personal circumstances change.

Importance of Asset Allocation and Equity Exposure

Asset allocation remains the primary driver of a portfolio27s risk and return characteristics. While retirees often reduce equity exposure, maintaining a portion in stocks is critical to counteract inflation. Historically, large-cap stocks have returned an average of 10.3% annually compared to 5.1% for government bonds.

Balancing equities and fixed income via a balanced growth and preservation approach ensures you participate in market upswings while limiting losses during downturns.

Liquidity Management and Cash Reserves

One of the most overlooked aspects of retirement planning is liquidity. By holding cash or short-term bonds covering one to four years of expenses, you limit the need to sell investments at depressed prices.

This strategy provides a buffer during market corrections, enabling you to follow through on planned withdrawals without panic and preserving the core of your portfolio for future growth.

Advanced Risk Mitigation Techniques

For sophisticated investors, hedging strategies can further protect against downside events. Options, futures, and inverse ETFs act as insurance policies during extreme market swings. However, these instruments carry complexity and potential costs.

Regular rebalancing restores your original risk profile by trimming outperforming assets and topping up those that lag, maintaining disciplined exposure to your target allocation.

Choosing Investment Vehicles

Mutual funds and exchange-traded funds (ETFs) simplify the execution of diversified strategies. They offer professional management, broad market access, and transparent fees.

Look for funds with low expense ratios and a track record of consistent performance. Avoid overconcentration in single holdings; instead, rely on low-cost diversified fund options that align with your risk and return objectives.

Monitoring and Adjusting Your Portfolio Over Time

Your retirement journey will span many years, during which market conditions and personal circumstances can shift significantly. Commit to at least annual reviews, with more frequent check-ups as you near critical milestones.

Revisit assumptions about longevity, spending needs, and market expectations. By integrating dynamic and personalized retirement plan adjustments, you ensure your portfolio remains aligned with your evolving life stage.

Preparing for Life Changes

Major events—such as marriage, health concerns, inheritance, or moving cities—inevitably influence your financial picture. Incorporate flexibility into your planning process to address these developments promptly.

Communicate with your financial advisor or trusted confidants to determine whether to shift allocations, update beneficiary designations, or adjust withdrawal rates. A proactive stance prevents reactive decisions driven by stress or uncertainty.

Conclusion: Building a Resilient Retirement Portfolio

Effective risk management in retirement hinges on balancing growth, income, and preservation. By understanding the key threats—overspending, excessive conservatism, unexpected plan deviations, and market downturns—you gain the clarity needed to navigate uncertainty.

Adopt a disciplined framework that includes diversification across multiple asset classes, prudent asset allocation, liquidity buffers, and regular rebalancing. When appropriate, consider advanced hedging techniques and professional fund management to fine-tune your protection.

Most importantly, keep your plan flexible to accommodate life27s inevitable changes. With these principles in place, you can face retirement with confidence, knowing your portfolio is prepared to withstand volatility and support your lifestyle goals for years to come.

References

- https://www.ml.com/articles/big-retirement-risks-and-how-to-prepare-for-them.html

- https://insight2wealth.com/blog/a-guide-to-balancing-risk-in-retirement-investments/

- https://www.nasdaq.com/articles/investment-strategies-retirees-balancing-risk-and-reward

- https://www.schwab.com/learn/story/ways-to-help-reduce-risk-your-portfolio

- https://realinvestmentadvice.com/resources/blog/investment-risk-management/

- https://www.investopedia.com/articles/financial-advisors/072915/what-does-ideal-retirement-portfolio-look.asp

- https://investor.vanguard.com/investor-resources-education/retirement/planning

- https://johnsonwim.com/balancing-risk-and-returns-in-your-retirement-portfolio